“Everything is awesome

Everything is cool when we’re part of a team

Everything is awesome

When we’re living our dream”

The theme song (at least the first line of it) from Warner Brothers 2014 surprise hit, The Lego Movie, is an apt illustration of our current market and economic situation. Everything is awesome. US construction spending increased to an all-time high of $1.25 trillion. Payrolls are increasing and unemployment has reached official levels only rarely seen in the past century. According to ADP and Moody's Analytics, private companies hired 234,000 jobs in January. This was well above expectations for 185,000. Service-related industries led with 212,000 new jobs; manufacturing added 12,000 and construction 9,000.

Not only are jobs being added, but wages are now increasing at the highest rate since 2008 (shown below in the rising Employment Cost Index YoY as calculated by Bloomberg).

Stock markets remain in one of the biggest bull markets in history. Over the past year, rising prices and optimism have surged to new highs. In fact just this week the Conference Board Consumer Confidence released data showing that the percentage of respondents who think the stock market will be higher this year reached an all-time record. Since the question was first asked back in early 1987, we can't look back any farther than 30 years with this data point. But this much is clear, at no time in recent decades have people been as bullish on stocks as they are today.

Everything is awesome, indeed!

If you've seen The Lego Movie (and we highly recommend it), you know that when everything is awesome, it might only be surface deep. That, in fact, is one of the main points of the wonderful satire. Smiley faces are not the same as deeply anchored joy. Bread and circuses (Starbucks, Netflix, and XBox?) are entirely different than independence, freedom, and opportunity. But, we digress.

As bond market maven, Jeffrey Gundlach (he of Bond King fame) succinctly pointed out this week, there is another way to look at things.

“Interest rates up, $ down, and mania sentiment everywhere...a dangerous cocktail.”

At the same time that stock markets and optimism have surged, interest rates have soared, inflation has gathered steam, and the international purchasing of the US dollar has fallen off the proverbial cliff. Why?

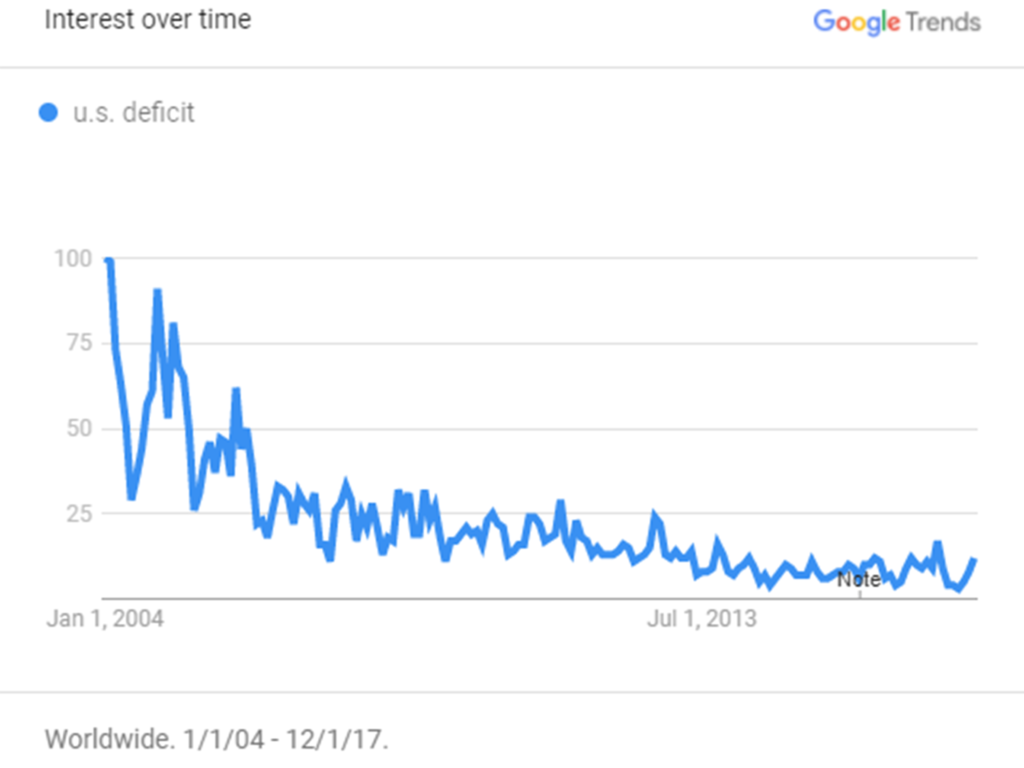

One reason is the long term structural concerns of the United States' fiscal position. This has recently been far from the radar of most casual economic observers. Do you even hear about budget deficits anymore? According to this chart of Google searches over the past decade, it has clearly fallen from public conscience.

Household Net Worth to US GDP

In 2017, the US Federal budget deficit was $700 billion in round numbers. The public debt surpassed $20 trillion. Only a few years ago, (2008) the debt surpassed $10 trillion for the first time. The budget deficit is expanding and doing so late in the market/business cycle which would typically be a period of decreasing deficit (and ideally a surplus). Under the new tax bill, this yawning discrepancy will grow by hundreds of billions.

Rising interest rates will likely have a significant additional impact. The Congressional Budget Office (CBO) estimates that for each percentage increase in interest rates, the deficit will rise by about $140 billion. This impact will be felt soon because about half of the debt matures in the next three years.

On top of that, there isn't much room for a reduction in total government spending without cutting welfare and other transfer program payments (and breaking the associated social contracts). 70% of federal spending is either interest payments or these transfer programs. (The largest remaining component, defense spending, appears more likely to increase than decrease in the current geopolitical environment.)

Additionally, a large amount of tax receipts are directly or indirectly related to rising asset prices. Capital gains account for about $0.20 of every tax dollar brought in by the Treasury. If asset prices were to stop rising (no decline necessary) then this alone would substantially impair the fiscal outlook.

In recent years, much of the debt financing was absorbed by the Federal Reserve (and other central banks) quantitative easing (QE) programs. As central banks shift policies away from bond buying (QE) to bond selling or balance sheet reduction known as quantitative tightening (QT), the net issuance of bonds that the rest of the market has to support increases dramatically. For example, the US net issuance of treasury bond in 2017 was $357 billion, but in 2018 is forecast by JPMorgan to increase to $828 billion.

The math fiscal math isn't pretty. Since the need for funding won't slow down, government borrowing will need to increase. This need to attract funds from lenders will put continued upward pressure on interest rates, downward pressure on the purchasing power of the dollar, or both. Financial assets are valued by projecting a future stream of income and then discounting these future dollars by an interest rate. Interest rates and currency concerns affect the value of them all.

(Additional investment specific commentary follows for client subscribers)

References:

https://www.cnbc.com/2018/01/31/private-jobs-up-234k-in-january-vs-185k-est-adp-moodys-analytics.html

https://www.bloomberg.com

http://tocqueville.com/tocqueville-gold-strategy-fourth-quarter-2017-investor-letter/

https://www.cnbc.com/2018/02/01/us-construction-spending-rises-as-private-outlays-hit-record-high.html

https://www.ft.com/content/8eae2e72-fb74-11e7-a492-2c9be7f3120a

https://www.etftrends.com/2018-outlook-for-equity-fixed-income-alt-investors/

SVANE CAPITAL, LLC IS A REGISTERED INVESTMENT ADVISOR. INFORMATION PRESENTED IS FOR INFORMATIONAL AND EDUCATIONAL PURPOSES ONLY AND DOES NOT INTEND TO MAKE AN OFFER OR SOLICITATION FOR THE SALE OR PURCHASE OF ANY SPECIFIC SECURITIES, INVESTMENTS, OR INVESTMENT STRATEGIES. INVESTMENTS INVOLVE RISK AND UNLESS OTHERWISE STATED, ARE NOT GUARANTEED. INTERNATIONAL INVESTING INVOLVES SPECIAL RISKS INCLUDING THE POSSIBILITY OF SUBSTANTIAL VOLATILITY DUE TO CURRENCY FLUCTUATIONS AND POLITICAL UNCERTAINTIES. AN INVESTMENT CONCENTRATED IN SECTORS AND INDUSTRIES MAY INVOLVE GREATER RISK THAN A MORE DIVERSIFIED INVESTMENT. THERE IS NO ASSURANCE THAT A DIVERSIFIED PORTFOLIO WILL PRODUCE BETTER RETURNS THAN AN UNDIVERSIFIED PORTFOLIO, NOR DOES DIVERSIFICATION ASSURE AGAINST MARKET LOSS. ANY GRAPH PRESENTED CANNOT IN AND OF ITSELF BE USED AS THE SOLE DETERMINANT IN MAKING AN INVESTMENT DECISION. GRAPHS ARE HISTORICAL DEPICTIONS AND HAVE INHERENT LIMITATIONS IN MAKING INVESTMENT DECISIONS AND CANNOT PREDICT THE FUTURE RESULTS OF ANY INVESTMENT. PAST PERFORMANCE IS NOT AN INDICATION OF FUTURE PERFORMANCE. BE SURE TO FIRST CONSULT WITH A QUALIFIED FINANCIAL ADVISER AND/OR TAX PROFESSIONAL BEFORE IMPLEMENTING ANY STRATEGY DISCUSSED HEREIN.